The Centrelink Age Pension Explained

Our Guide To Centrelink Age Pension

Am I Eligible For The Age Pension?

If you have reached Age Pension age (see table below) and been an Australian resident for at least 10 years, you may be eligible to receive Centrelink Age Pension entitlements or other Government benefits. The amount of pension entitlement you may receive will depend on a number of factors including your family situation (single or couple), your level of income and assets and if you are a homeowner or non-homeowner.

Income Test

The Centrelink income test generally includes any income you earn from any source, including employment income, Australian and overseas pensions and investment income (such as net rental income). When assessing income from some investments assets (including superannuation and account based pension balances) Centrelink will apply a deemed rate of income.

Asset Test

If you are a homeowner the family home is exempt under the assets test. Centrelink will assess any other assets you own, including overseas assets. This includes your home contents and motor vehicles, savings and investments such as term deposits and shares, investment properties and monies inside the superannuation environment. Centrelink will generally assess assets at current market value and deduct any debt you hold against applicable assets such as a loan on an investment property.

For couples, Centrelink will look at your combined income and assets position. The test that results in the lowest pension rate is the one Centrelink will use to determine your entitlements.

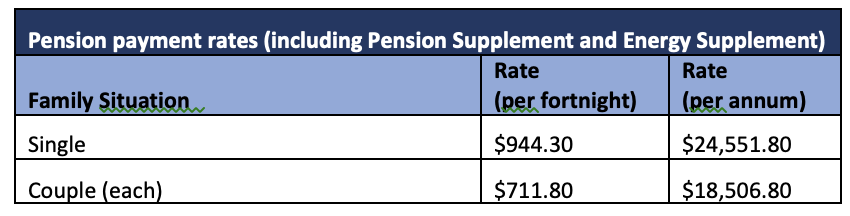

How much will I get?

The maximum Age Pension rate you can receive (between 1 July 2020 - 19 September 2020) is:

Even if you don’t qualify for a full Age Pension, you may be entitled to a part Age Pension and/or access other payments and benefits such as Commonwealth Seniors Health Card, Pensioner Concession Card, Pension Supplement and Rent Assistance.

Strategies to help maximise entitlements

Around 65% of people in retirement rely on some form of Government pension or allowance as their main source of income. Strategic advice can play a significant part to ensuring you can maximise your Centrelink position.

Member of Couple (Superannuation)

Generally super in accumulation phase for someone under Age Pension age is an exempt asset and only becomes assessed once you have reached Age Pension age. One common strategy is when one member of a couple has reached Age Pension age, withdraws and recontribute their super to the younger spouses super account in accumulation phrase, which is not assessable until they reach their Age Pension age. This strategy can see some couples receive immediate access or increase in Age Pension entitlements. Seeking advice prior to implicating this strategy is paramount as there are preservation and contributions limits that may apply.

Gifting

Gifting is a strategy some clients use to improve their Centrelink Age Pension entitlements. The allowable limit for gifting is $10,000 in each financial year or $30,000 over a 5-year rolling period. Any amount above these limits will be assessed under the income and assets test.

Lifetime Annuity

Investing a portion of your portfolio in a lifetime income stream may provide an instant reduction in the assessable assets included for the calculation of your Centrelink entitlements. With regards to the assets test only 60% of the purchase amount is assessed as an asset until age 84, or for a minimum of 5 years. This reduces to 30% of the purchase amount for the rest of your life. Not only does a lifetime annuity potentially provide better Centrelink outcome but it also provides a guaranteed regular income for your lifetime which will not be impacted by market movements. This provides certainty for many clients and peace of mind that together with their increased Centrelink entitlements, superannuation or investments and savings, they are able to meet their retirement income objectives throughout retirement.

As always, thank you for your continued trust and confidence.

Warm regards,

Damian and Chanthy